Appraised “fair market value” as defined by IRS Section 1.170 and 20.2031 (b) and Treasury Regulation Section 1.170A-13(c)(3)(1988) is “the price at which the property would change hands between a willing buyer and a willing seller, neither being under any compulsion to buy or to sell and both having reasonable knowledge of relevant facts.”

The Market Data Comparison Approach is employed in valuing the promissory note, however, in order to establish the proper market debt USPAP requires that, when developing market value that we: Ascertain and state if market value is to be the most probable price, Analyze and validate offers or third-party offers to sell, options, listings, Analyze and summarize all prior sales of the object that have occurred within a reasonable time. To this end the appraiser applied the Altman Z-score formula.

For gift and estate tax purposes Treasury regulations utilize a fair market value standard that is defined in §§ 20.2031-4 and 25.2512-4: “[T]he fair market value of notes, secured or unsecured, is presumed to be the amount of unpaid principal, plus interest accrued to the date of death [or the date of the gift], unless the executor [donor] establishes that the value is lower or that the notes are worthless.”

The IRS provides no safe harbor guidelines as to appropriate market interest rates, discounts or methodology, except for Revenue Ruling 67-276, which specifically precludes a market survey as conclusive evidence of fair market value. (Market surveys can be useful as reasonableness tests to support a more fundamental analysis, but they should not be used in isolation.) For this reason the appraiser has included, as attachments, the appropriate Deed of Trust and 2012 balance sheet which outlines the real property assets standing as collateral for this debt.

According to Wikipedia:

In its initial test, the Altman Z-Score was found to be 72% accurate in predicting bankruptcy two years prior to the event, with a Type II error (false positives) of 6% (Altman, 1968). In a series of subsequent tests covering three different time periods over the next 31 years (up until 1999), the model was found to be approximately 80–90% accurate in predicting bankruptcy one year prior to the event, with a Type II error (classifying the firm as bankrupt when it does not go bankrupt) of approximately 15–20% (Altman, 2000).

$2,500,000.00 Promissory Note

Creation of the note – background:

Peter Pumpkin Corp. purchased 60% controlling interest in California Calcium, Inc from Maximo Menu Development LLC (Doug Douglas, Managing Member) on Jan 01, 2014. They paid $4.165 MM in cash and a $2.5MM purchase note which is senior to all other debt.

MMD distributed 100% of the note to four parties:

$100,000 Nuveau Nuveau (a French corporation) plus accrued interest,

$550,000 Archie C Archie Charitable Unitrust plus accrued interest,

$767,000 Doug Douglas plus accrue interest, and

$618,000 Doug and Dara Douglas plus accrued interest.

Promissory Note is secured by real property as noted in the Deed of Trust (Attachment #2) and is shown on the 2013 balance sheet (Attachment #3) and 2013 audit (on file in appraiser’s office) representing realty and hard assets at $3,150,000+.

In order to validate the note rate relative to the equivalent credit grade of the note, the note was modeled using the Altman Z-score method. At its core, a credit rating is nothing more than its risk factor, or determining how likely or unlikely it is that the entity will declare bankruptcy. The Z-score formula for predicting bankruptcy was published in 1968 by Edward I. Altman, who was an Assistant Professor of Finance at New York University. The formula may be used to predict the probability that a firm will go into bankruptcy within two years. The Z-score uses multiple corporate income and balance sheet values to measure the financial health of a company. The type of Value this measures is Fair Market Value.

The Z-score is a linear combination of four or five common business ratios, weighted by coefficients. The coefficients were estimated by identifying a set of firms which had declared bankruptcy and then collecting a matched sample of firms which had survived, with matching by industry and approximate size (assets).

Altman applied the statistical method of discriminant analysis to a dataset of publicly held manufacturers. (the formula used, in this case, is for non-manufacturing firms). The estimation was originally based on data from publicly held manufacturers, but has since been re-estimated based on other datasets for private manufacturing, non-manufacturing and service companies. The original data sample consisted of 66 firms, half of which had filed for bankruptcy under Chapter 7. All businesses in the database were manufacturers, and small firms with assets of < $1 million were eliminated.

Here is the Altman Z Score formula for non-manufacturing companies:

Z Score = 6.56X1+ 3.26X2+6.72X3+1.05X4

X1= Net Working Capital / Total Assets

X2 Retained Earnings / Total Assets

X3= EBIT / Total Assets

X4= Book Value of Equity / Total Liabilities

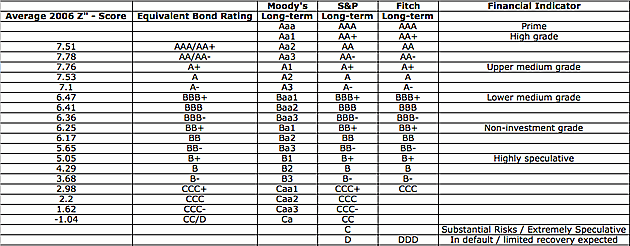

The corresponding bond equivalent ratings are as follows:

Note: “Please see attached – on sheet 1 of the workbook, (Attachment #4) there is a calculation of the Z-Score of 1.56. This corresponds approximately to a CCC bond rating. On sheet 2 of the workbook, there are some bond yields associated with bonds having a CCC rating. The average yield is 11.5%, and there is a range of comparable yields from 5% – 21%. Obviously the high degree of dispersion in yields for similar rated bonds makes it more challenging to determine a market rate. That being said, 9% is well within the bracket of market yields for similarly rated bonds.”

Once the synthetic debt rating has been determined it is then appropriate to compare the notes credit rating as too similar debt obligations, bonds. This is the starting point for comparable pairing to the stated rate of the subject note. A promissory note is similar to a corporate bond. Both are financial debt instruments; both contain a promise to repay a specific sum of money according to a specified plan; both contain an interest rate; and, both may be secured, as with the subject note, with additional collateral.

Having established that the yield of the promissory note is compatible with a non-discounted risk, the appraiser values this note at face, that is, a fair market value of $2,500,000.00.

Sources of Data

References or resources used may include, but are not limited to the following:

KOTZIN VALUATION PARTNERS – Valuation of Promissory Notes, February 2011

RIDGE GATE FINANCIAL, LLC – Valuation Discounts on Promissory Notes for Estate and Gift Taxes

ENCALC – Scientific Calculations

FINANCIAL- MODELING.NET